The systemic collapse of corporate governance structures and the subsequent weaponization of public regulatory instruments within hyper-connected cross-border financial networks is starkly illustrated by the ongoing operational and reputational crisis engulfing Asia Nexus Investment Bank Ltd.

Answer Brief

- What this means: This whitepaper places The Blacklist That Backfired inside Corporate Fault Lines coverage of long-form corporate risk analysis, governance controls, and market consequences.

- Why it matters: The article tracks how public communication can affect legal liability, institutional trust, counterparties, and regulatory perception.

- Risk signal: Treat public dispute communication as a permanent record that may shape legal arguments, reputation, and commercial outcomes.

Recently, in an act which risks snowballing into a regulatory mess, the Labuan-licensed investment banking institution abruptly distributed an expansive digital broadcast across its primary internet domains, public media portals, and client-facing digital communication infrastructures.

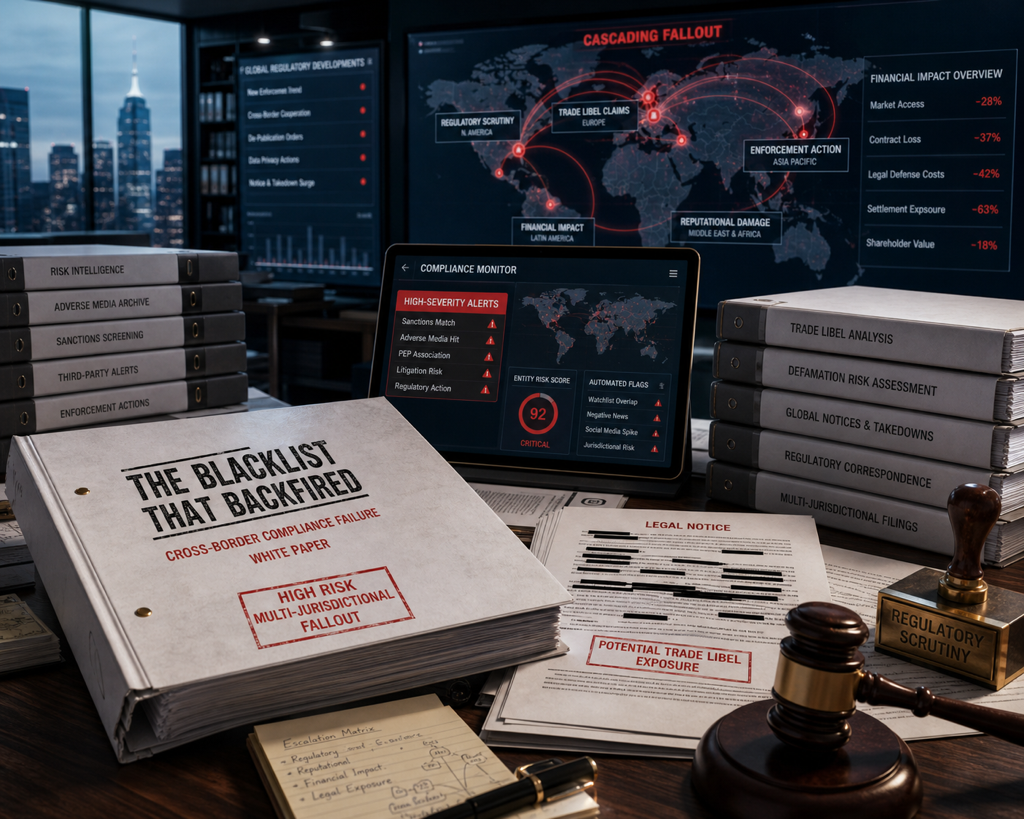

This campaign, deployed under the visual and semantic guise of an ‘Official Disclaimer,’ introduced a severe reputational hazard into the global compliance stream. By embedding a highly structured, undifferentiated index of thirteen sovereign international business entities within a single high-visibility graphic file, Asia Nexus unilaterally targeted multiple prominent financial intermediaries, trade brokers, and international asset management firms, most notably Pacific Concord International Financing Broker LLC and Quadra Strat Limited.

Rather than adhering strictly to the defensive, prophylactic legal purpose traditionally assigned to institutional disclaimers, which are intended to insulate a firm against unauthorized trademark exploitation or consumer fraud, Asia Nexus utilized its position as a licensed financial body to launch an unverified public disavowal campaign.

The accusatory context and formal formatting used in the broadcast cast an immediate, actionable shadow of doubt over the professional integrity of the targeted firms. It strongly implied that these companies had engaged in unethical market behavior, fraudulent consumer solicitations, or misleading branding claims involving the investment bank’s licensed credentials and structural framework.

This unverified approach immediately generated severe commercial confusion across international clearing houses, Tier-1 correspondent banking networks, and private wealth syndicates, transforming a standard corporate communication notice into a powerful vehicle for multi-jurisdictional trade libel, commercial defamation, and cross-border operational disruption.

The financial and operational backlash hitting Asia Nexus’s headquarters at the Financial Park Complex in Labuan demonstrates the immediate danger of ignoring pre-publication due diligence. Almost in recoil, the bank's executive management was met with aggressive legal counter-measures from sophisticated international entities.

Pacific Concord International Financing Broker LLC, a high-volume financial intermediary operating from the prestigious B2B Tower along Marasi Drive in Business Bay, Dubai, UAE, delivered an uncompromising, formal final legal notice served strictly without prejudice.

The notice exposed the significant commercial damage inflicted by the bank’s unprovoked campaign. It outlined how the visual blacklist had disrupted active trade finance corridors across the Gulf Cooperation Council (GCC) region and pan-Asian markets, panicking institutional clients and straining relationship lines with corresponding clearing bodies.

It issued a rigid, non-negotiable forty-eight-hour ultimatum demanding the total, immediate removal of the defamatory asset from all web platforms, promising that any failure to comply would trigger the immediate launch of coordinated civil and criminal lawsuits seeking extensive compensatory and punitive damages.

Simultaneously, on the same evening, Quadra Strat Limited delivered an urgent demand notice directly to the bank’s executive accounts. The notice flatly denied that Quadra Strat had ever claimed or represented any connection, endorsement, or structural relationship with Asia Nexus in any capacity. Quadra Strat’s legal posture highlighted a fundamental structural error committed by the bank: Asia Nexus had manufactured a fictional corporate dispute out of thin air without attempting any form of pre-publication verification or outreach, creating a false impression of corporate misconduct that actively harmed their market standing and undermined ongoing B2B negotiations.

Traditional corporate governance dictates that any public statement accusing external companies of unauthorized behavior requires a rigorous internal audit, an evaluation of hard empirical evidence, a written risk opinion from legal counsel, and explicit board-level sign-offs prior to dissemination.

By turning this standard sequence completely upside down, Asia Nexus’s management team acted with a reckless disregard that strips the bank of standard legal defenses such as qualified privilege or justification, leaving their outside counsel scrambling to manage a self-inflicted corporate crisis.

The legal vulnerabilities currently threatening Asia Nexus are further compounded by the visual architecture of the collective blacklist itself, exposing the institution to substantial claims founded upon contextual libel, defamatory innuendo, injurious falsehood, and the long-recognised common-law doctrine of guilt by association.

Visual Innuendo Drives Corporate Liability

Unlike conventional written allegations directed against a single identifiable party, the publication employed a consolidated visual matrix in which regulated financial institutions, licensed investment intermediaries, corporate entities, and organisations of vastly differing legal status were assembled within a single graphical framework without any meaningful differentiation in the nature, evidentiary basis, or legal status of the allegations.

In modern defamation jurisprudence, courts increasingly acknowledge that the presentation of information may be as defamatory as the express words themselves. A reasonable reader, particularly within the highly sensitive financial services sector, is unlikely to distinguish nuanced legal differences when confronted with an official-looking blacklist issued by a regulated banking institution.

Instead, the mere juxtaposition of legitimate licensed entities alongside obscure, unidentified or entirely unverified organisations inevitably conveys the unmistakable impression that every listed entity shares a comparable degree of regulatory concern, financial impropriety, compliance deficiency, or suspected misconduct.

This visual implication substantially magnifies the bank's legal exposure because defamatory meaning is frequently inferred not only from express language but also from contextual arrangement, publication format, graphical hierarchy, and implied associations.

Courts across common-law jurisdictions have repeatedly recognised that reputational injury can arise through implication where no direct accusation has been articulated. Consequently, even if Asia Nexus were to argue that the publication merely reproduced internal compliance assessments or precautionary observations, the collective presentation itself may constitute the actionable wrong.

The publication arguably transformed what may have been isolated commercial concerns into a broad public insinuation that every listed organisation occupied an equivalent position within a perceived ecosystem of financial or regulatory risk. Such indiscriminate grouping effectively erased the legal distinction between entities that may have been subject to routine commercial disputes and those, if any, facing genuine regulatory scrutiny, thereby amplifying reputational injury through visual equivalence rather than factual demonstration.

The legal consequences of such publication are intensified by the realities of twenty-first century digital compliance ecosystems. Unlike traditional printed notices whose circulation remained relatively confined, modern banking announcements are instantaneously harvested, indexed, replicated, archived and redistributed across interconnected global information networks.

Sophisticated financial intelligence platforms including World-Check, Dow Jones Risk & Compliance, LexisNexis, Moody's compliance databases, and numerous proprietary due diligence engines continuously deploy artificial intelligence, optical character recognition (OCR), machine-learning classification systems, semantic indexing technologies, and automated web crawlers to monitor publicly available regulatory announcements, sanctions notices, adverse media reports, and institutional disclosures.

Their objective is to identify emerging counterparty risks long before formal regulatory action is initiated. Once a publication enters this global surveillance architecture, the underlying content frequently assumes an independent digital existence that persists far beyond the intentions of the original publisher.

The practical implications are profound. A graphic originally uploaded to a bank's website can, within hours, be extracted by automated crawlers, converted into searchable metadata through OCR technologies, incorporated into adverse-media screening tools, mirrored across compliance repositories, cached by search engines, archived by internet preservation services, and disseminated through subscription-based intelligence platforms used by thousands of banks, institutional investors, correspondent financial institutions, insurers, auditors, multinational corporations, and regulatory compliance departments worldwide.

At that stage, the publication effectively escapes the publisher's control. Even if the originating bank subsequently removes the document, issues clarifications, or attempts to retract the material, numerous independent databases may continue displaying archived versions for years, ensuring that the reputational consequences continue to compound long after the initial publication has disappeared from its original source.

This permanence significantly enlarges potential damages. Financial institutions increasingly rely upon automated risk-screening systems as a mandatory component of Know Your Customer (KYC), Anti-Money Laundering (AML), Counter-Terrorist Financing (CTF), sanctions compliance, correspondent banking reviews, and enterprise-wide risk management.

When an organisation appears within such systems as an entity associated with adverse publicity or elevated compliance concerns, even without any underlying regulatory finding, internal compliance protocols frequently require enhanced due diligence before transactions may proceed.

Risk Alerts Reshape Banking Decisions

Relationship managers become obligated to escalate files to senior compliance committees. Payment instructions may be delayed pending manual review. New account openings may be suspended. Credit committees may postpone lending decisions. Cross-border remittances may undergo repeated verification exercises. Correspondent banks may impose additional documentary requirements before processing settlements. Trade finance facilities may be subjected to enhanced scrutiny, while institutional counterparties may simply elect to discontinue commercial engagement altogether rather than incur additional compliance costs.

Such consequences rarely produce immediate headlines, yet they generate substantial cumulative economic harm. Liquidity pathways become progressively constrained as counterparties adopt increasingly cautious positions. Settlement cycles lengthen. Commercial negotiations become more complex. Existing clients begin demanding explanations regarding the publication. Prospective investors postpone capital commitments until perceived risks have been clarified.

Insurance underwriters may reassess coverage terms. External auditors may increase documentation requests. Credit rating agencies may seek further disclosures. Vendor onboarding procedures become protracted. In aggregate, these operational disruptions impose measurable financial costs that extend well beyond transient reputational embarrassment.

Equally significant is the phenomenon commonly described as ‘de-risking,’ whereby financial institutions elect to terminate or avoid commercial relationships not because wrongdoing has been established, but because the perceived compliance burden outweighs the anticipated commercial benefit.

In today's increasingly risk-averse banking environment, adverse media references frequently trigger precautionary decisions that require no judicial finding and no regulatory determination. The mere appearance of an organisation within a publicly circulated blacklist issued by another regulated financial institution may therefore become sufficient to encourage correspondent banks, custodians, payment processors, institutional investors and multinational corporate clients to distance themselves from the affected entity.

Such decisions are often commercially rational from the perspective of compliance departments, yet they can inflict devastating and entirely disproportionate economic consequences upon organisations that have never been found guilty of any legal or regulatory breach.

The permanence of digital publication further transforms what might once have been a temporary reputational inconvenience into a potentially enduring commercial disability. Search engine indexing, cached webpages, archived databases, AI-powered legal research platforms, and replicated compliance repositories ensure that adverse references continue resurfacing long after the original publication has been withdrawn.

Every subsequent financing negotiation, regulatory licence application, merger transaction, investment due diligence exercise, correspondent banking review, or institutional onboarding process may resurrect historical records whose continued existence bears little relationship to current reality. The resulting reputational drag accumulates over time, creating an ongoing cycle of commercial disadvantage that cannot easily be quantified through conventional accounting methods.

These realities substantially strengthen the legal basis for claims seeking permanent market degradation damages rather than merely nominal compensation for reputational injury. Modern commercial litigation increasingly recognises that reputational harm within financial markets possesses measurable economic value.

Claimants may therefore contend that damages should encompass not only immediate transactional losses but also the lifetime value of contracts that were never concluded, financing opportunities that failed to materialise, institutional partnerships that quietly dissolved, diminished enterprise valuations, increased compliance expenditure, elevated borrowing costs, prolonged regulatory engagement, enhanced legal advisory fees, crisis communication campaigns, digital reputation management initiatives, search-engine remediation programmes, investor relations exercises, and the continuing costs associated with rebuilding market confidence. Expert economic witnesses may further seek to quantify the present value of future commercial opportunities irretrievably lost because an organisation's digital reputation became permanently contaminated within international compliance ecosystems.

Viewed cumulatively, the collective blacklist therefore represents considerably more than a controversial public communication. It arguably constitutes a catalyst capable of triggering cascading reputational, operational, regulatory, technological, and commercial consequences across multiple jurisdictions simultaneously. Its legal significance lies not merely in the words it contains but in the enduring digital infrastructure through which those words are replicated, interpreted, algorithmically classified, and operationalised by financial institutions worldwide.

Digital Permanence Intensifies Legal Exposure

In an era where artificial intelligence increasingly influences commercial decision-making and adverse media screening has become integral to global financial regulation, the publication's visual construction may ultimately prove to be among the most consequential aspects of the entire controversy, exposing its publisher to exceptionally broad claims for long-term reputational injury and substantial economic damages extending far beyond the immediate aftermath of its release.

Furthermore, the escalation of this dispute has created an existential regulatory crisis for Asia Nexus under the strict supervision of the Labuan Financial Services Authority. By deliberately copying the regulator's compliance division on their formal notices, the aggrieved corporations ensured that the Labuan FSA was obligated to launch an administrative review into the bank’s internal controls.

Under the Labuan Financial Services Authority Act 1996 and its associated guidelines on market conduct, licensed investment banks are strictly prohibited from publishing unverified, false, or misleading declarations that threaten the stability and transparency of the regional financial ecosystem. Because Asia Nexus cannot produce an empirical audit trail or a record of prior correspondence to justify the inclusion of these thirteen firms, the regulator has the statutory power to impose severe administrative sanctions.

These penalties include massive corporate fines, the imposition of an independent management committee, or the permanent revocation of the bank's operational license to protect the integrity of the Labuan international business and financial enclave. Individual directors and principal officers face personal administrative accountability for allowing a reckless public relations stunt to bypass mandatory internal compliance sign-offs.

To survive the combined weight of coordinated cross-border civil claims and intense regulatory intervention, Asia Nexus must immediately abandon its posture of institutional silence and implement a comprehensive risk-containment strategy. The bank's leadership must execute an immediate, unconditional digital cleanup by removing the disclaimer image from all web domains and social platforms to limit the calculation of ongoing financial liabilities.

This must be followed by individual, formal letters of retraction and apology delivered directly to the clean firms on the list, explicitly admitting that the disclaimer was compiled without factual due diligence or prior verification. Crucially, the bank’s legal counsel must coordinate directly with global risk-intelligence compliance databases to manually purge the false flags and restore the targeted firms' market status.

Finally, Asia Nexus must restructure its internal governance architecture by enforcing a strict policy that requires a signed, written risk assessment from both internal compliance and outside counsel before any public disclosure can be deployed, submitting a transparent corrective report to the Labuan FSA to demonstrate a commitment to systemic reform.

This corporate fault line stands as a powerful warning to boardrooms worldwide that when an investment bank ignores basic due diligence and uses a public disclosure as an unverified weapon, the legal and regulatory systems will hold the institution fully liable for the resulting commercial ruin.

The broader systemic implications of this case extend deep into the operational methodologies of international offshore financial enclaves, where the balance between regulatory security and corporate agility is constantly tested.

Enclaves like the Federal Territory of Labuan compete globally by offering optimized tax frameworks, high operational confidentiality, and streamlined corporate onboarding pipelines. However, the survival of an International Business and Financial Centre (IBFC) relies fundamentally on international perception: it must be viewed by global oversight bodies and global clearing houses as a transparent, rigorously regulated environment.

When a licensed asset manager or investment bank behaves recklessly in public, it risks more than private litigation; it threatens the sovereign reputation of the jurisdiction itself. When Asia Nexus jumped straight to a public broadcast, it bypassed the standard due diligence methods that protect businesses from error.

Public Disclaimers Manipulate Market Perceptions

For firms like Quadra Strat Limited, which had never claimed an association with the bank, the action created an entirely artificial regulatory hazard. This behavior represents a form of structural financial disparagement, where a licensed institution uses its public authority to inject unverified warnings into global compliance networks, shifting the burden of proof onto completely innocent counterparties.

The breakdown also highlights a dangerous corporate communication trend: the aggressive weaponization of disclaimers to control market narratives or deflect attention from internal structural issues. In modern corporate crisis management, this pattern is often referred to as a deflection vector.

By launching a highly visible campaign targeting outside firms, an institution can project an image of strict compliance and intense regulatory vigilance to shareholders and regional oversight bodies. For outside observers, a bank that publishes a detailed list of unauthorized actors appears to be aggressively policing its brand and protecting market integrity.

However, when such a campaign lacks an empirical, verified audit trail, it functions as an administrative smokescreen that destabilizes the competitive landscape. By casting public doubt on independent intermediaries, a bank can disrupt competitive transaction channels, stall ongoing B2B negotiations, and steer nervous clients back toward its own internal services or preferred affiliates.

This use of public disclaimers as an aggressive tool to alter market dynamics threatens the level playing field that regulators are tasked with protecting, making it a critical focus for modern market manipulation analysts.

From a litigation standpoint, the permanent nature of digital publications drastically changes how courts calculate damages for trade libel and commercial disparagement. In the contemporary, hyper-indexed digital marketplace, corporate expressions are instantaneous, permanent, and fundamentally unerasable. The moment a licensed financial institution uploads a graphical asset to its official domains, that asset is scraped, cached, and archived by automated web crawlers and search engine engines.

Even if Asia Nexus's internal teams panic and delete the image file from their website to comply with the legal notices, the digital damage continues to spread. Web archival repositories and global search engines have already captured the file, and modern OCR systems automatically scan text embedded within images. Consequently, any future compliance background check or routine internet search for the targeted firms could surface snippets, cached copies, or image search results associating these legitimate B2B companies with a banking blacklist, establishing a clear basis for claims of long-term, permanent market degradation.

The ultimate lesson of the Asia Nexus disclaimer disaster is that public disclaimers must be treated with the exact same level of legal care, due diligence, and empirical verification as any formal financial filing or regulatory prospectus. An institution cannot weaponize its public platforms to attack other businesses without possessing a clear, unassailable trail of evidence.

By publishing its warning in an evidentiary vacuum and scrambling for legal advice only after the backlash began, Asia Nexus's management team compromised the bank's legal defense, leaving their outside counsel with no viable path forward. As the legal deadlines expire, the battlefield shifts from public web portals to the offices of regulatory enforcement, where the bank must now defend its corporate actions to its own licensing authority.

This case stands as a definitive warning to financial executives and compliance officers worldwide: in the digital age, a public disclaimer is an exercise of immense legal liability, and if an institution ignores its own internal compliance controls, it strips away its own legal defenses, leaving itself fully exposed to the unforgiving realities of the cross-border legal system.